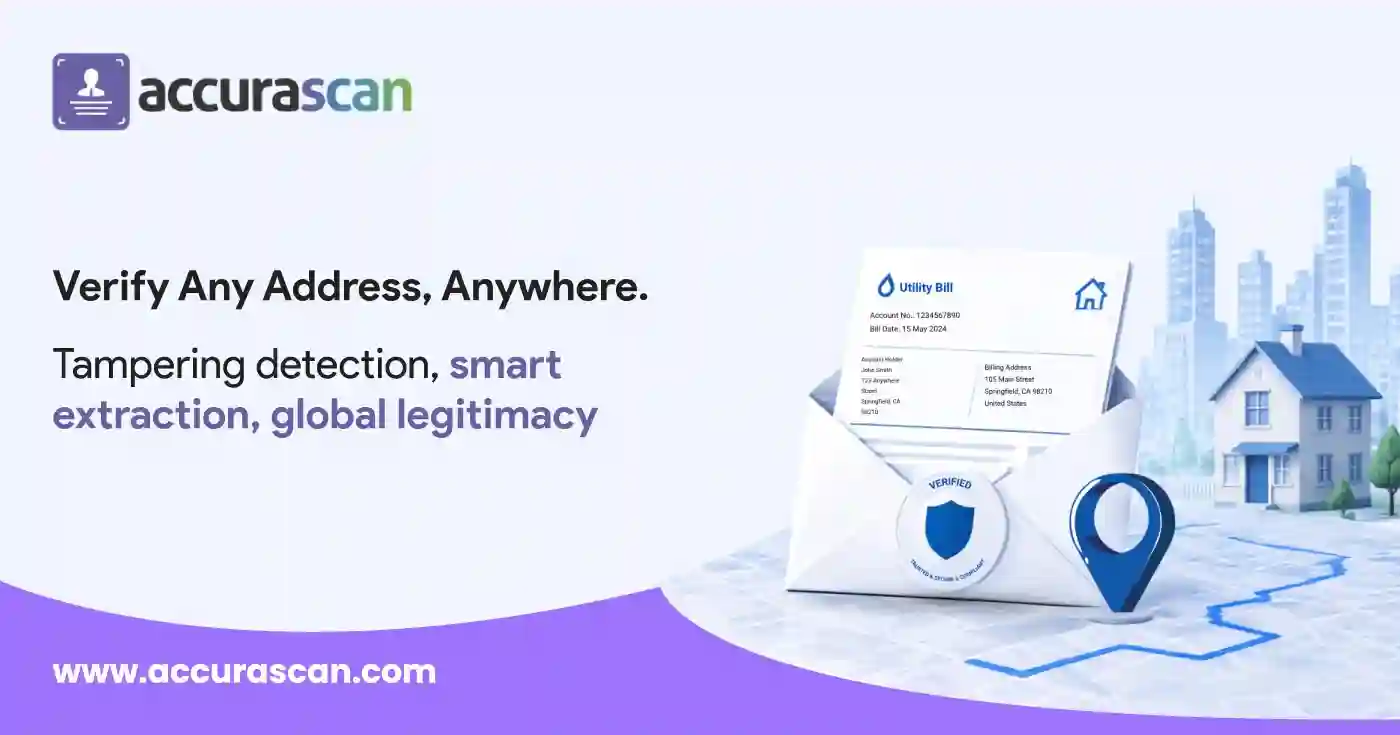

Ask any KYC operations head where their fraud losses come from, and the answer is almost always the same: address proof.

It’s the softest target in the entire onboarding stack. A passport has a chip. Other cards have a hash. An address proof is just a PDF. And a PDF can be edited by anyone with a free trial of Acrobat.

Worse: even if the document is real, the address on it might not be. Streets that don’t exist. PIN codes that don’t match cities. Buildings that were demolished a decade ago. Most KYC workflows have no way to tell.

Proof of Address was built to fix exactly this.

One upload. Multiple forensic checks. A single, structured verdict — delivered in under a second.

Why Address Verification Keeps Breaking

Walk through a typical KYC funnel and you’ll see the same pattern repeat across banks, lenders, wallets, and brokerages:

- A user uploads a utility bill.

- A reviewer opens it.

- They squint.

- They check the name.

- They check the address roughly matches what the user typed.

- They click approve.

That’s it. That’s the verification.

No tampering check. No structural analysis. No real-world validation of whether the address actually exists. Just a human, a screen, and a guess.

Multiply that across millions of onboardings a year, and the math gets ugly fast:

- One in every few hundred documents is forged outright

- A smaller fraction contains real documents with edited fields

- And a meaningful slice contains addresses that look plausible but don’t exist in any geographic dataset

Each one of those is a regulatory finding waiting to happen.

Each one is a synthetic-identity loan waiting to default.

Each one is a fraud team escalation that someone, somewhere, has to clean up.

The Multi-Layer Approach

Most vendors solve one piece of this puzzle. We built Proof of Address to solve all sequentially, in one API call, with one verdict at the end.

Step 1: Is the Document Real?

Before we even read the address, we look at the document itself.

Metadata, fonts, edit history, image compression patterns, structural integrity — the same forensic signals a digital examiner would check, run automatically in milliseconds.

If someone has tampered with the file, we know.

Often we can tell exactly which field was changed.

Step 2: What Does It Say?

Address documents are messy.

Different layouts. Bills folded into PDFs with logos and barcodes and disclaimers.

Our extraction engine reads through all of it and returns the address as clean, structured data — line by line, normalised to local conventions, ready to flow into your KYC system without a human ever retyping it.

Step 3: Does the Address Actually Exist?

This is the step nobody else does well.

We validate the extracted address against authoritative global address datasets — confirming the street exists, the postal code is real, the city matches the country, and the geography lines up with what the user claims.

A bill that passes the first two checks but fails the third? That’s a fraudster who knows how to forge a document but doesn’t know your local geography.

We catch them at step three.

Who’s Using It

Proof of Address sits inside onboarding flows for:

- Banks and neo Banks — slotting into account opening between document upload and KYC review

- Lenders and BNPL platforms — validating address before disbursal to cut first-party fraud

- Crypto exchanges and wallets — strengthening CDD evidence in front of FATF and MiCA examiners

- Reg Tech platforms — embedded as a microservice inside larger KYC orchestration stacks

- Insurers and brokerages — used at policy issuance, Demat opening, and claims intake

- Telecom operators — verifying address during SIM and broadband onboarding

The pattern is the same everywhere:

- Replace the squinting reviewer with a structured, audit-ready verdict.

- Free the humans to handle the edge cases.

- Let the machine handle the volume.

What You Get in the Response

One call. Four things back:

- A tampering verdict, with field-level evidence if applicable

- The extracted address

- A legitimacy result, validated against global datasets

That’s it.

No orchestration logic to write.

No second vendor to integrate.

No data cleaning step on your side.

If the document is clean, the address is correctly extracted, and the legitimacy check passes — you get a green light and a structured payload.

If any of the layers fail, you get a specific, defensible reason why.

The Bigger Point

KYC stacks have been over-engineered everywhere except the place where most fraud actually happens.

Banks spend millions on liveness checks, biometric matching, and identity decision engines — then accept a forged PDF of an electricity bill at face value because nobody built the tooling to verify it.

Proof of Address is that missing tool.

It won’t replace your KYC orchestrator.

It won’t replace your liveness vendor.

It’s not trying to.

It’s trying to close the one open door that fraud teams have been quietly losing money through for the past decade.

Key Takeaway

- One document.

- Multiple checks.

- Zero guesswork.

That’s the bar address verification should have been held all along.